Via blog.VariantPerception.com,

The main downside risk today that the market may not fully appreciate is the reversal of the historically large post-Covid bullwhip effect, which pulled forward a lot of future demand.

The bullwhip effect started with surging consumer goods demand and led to a huge restocking impulse up the supply chain. The below is an excerpt from our July 19th report.

As we highlighted in our July Macro Snapshot:

“ISM new orders to inventory ratio has been collapsing, suggesting this is the beginning of the end of the bullwhip effect. The significant build-up of US retailer inventories is set to exert a strong deflationary force on the economy once the bullwhip effect reverses.”

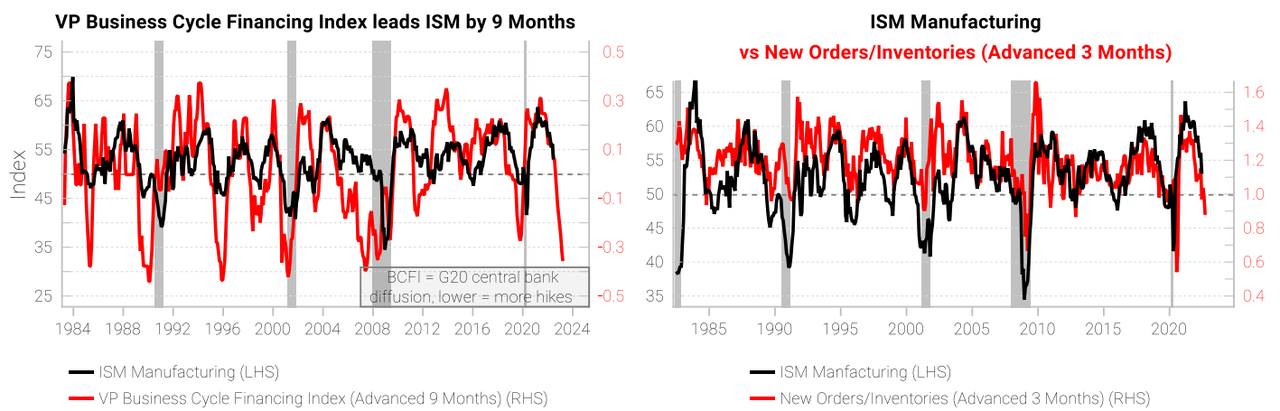

Leading relationships for ISM manufacturing are bad and still deteriorating.

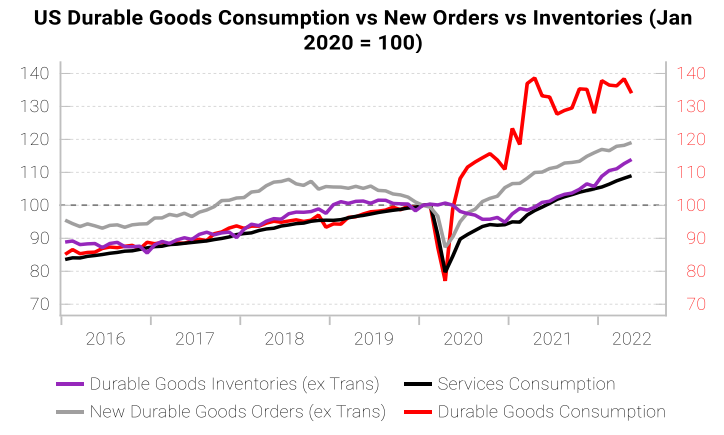

We are tracking “hard” data to confirm the message from LEIs and the intensity of the industrial slowdown. Absolute USD values of manufacturing new orders and durable goods consumption are still elevated compared to pre-pandemic levels.

More timely hard data confirms the industrial slowdown has started.

Production at US factories declined in June for a second month owing to higher inventories and total industrial production fell for the first time this year (link).

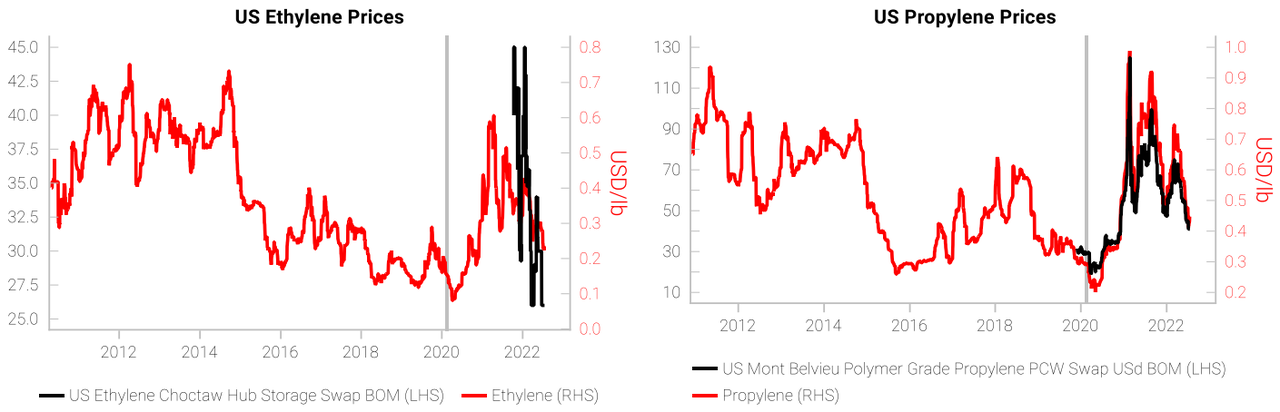

Chemical prices have weakened significantly, signaling falling demand in the face of high prices and weakness in downstream markets. (Ethylene and propylene are key inputs for plastic and household chemical compounds).

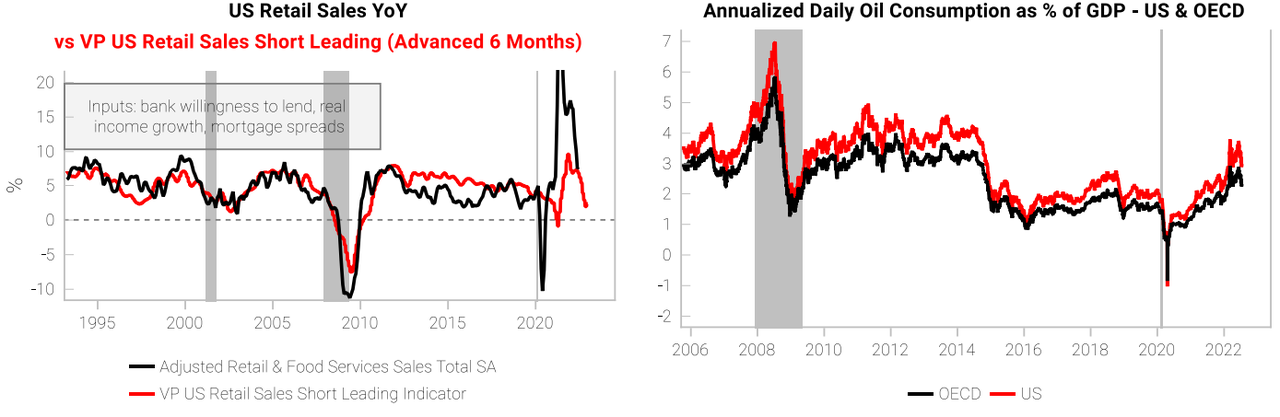

Retail sales growth has moderated and has closed the divergence with our retail sales LEI.

We expect further weakness ahead (left-hand chart). Oil consumption as % of GDP has fallen sharply suggesting US consumer resilience is cracking.

* * *

Get the full picture at variantperception.com