Submitted by QTR’s Fringe Finance

“I’m not going to sit on my ass as the events that affect me unfold to determine the course of my life. I’m going to take a stand. I’m going to defend it, right or wrong, I’m going to defend it.”

– Cameron Frye

My paid subscribers know we were pretty much spot on in predicting that the 9.1% CPI print from last month (1) marked the short term CPI peak and that (2) equity markets would rally in the short to mid-term as a result. I predicted it would happen in my July 2022 portfolio update:

I think it’s likely the 9.1% print is the peak, for a little while at least, based on current spot prices. Used cars are down, new cars are down, home prices are starting to come down as more inventory comes on the market, oil has sold off over the last 2 weeks, etc. This doesn’t mean inflation is over, not does it mean stocks won’t still move lower in the longer term once the effect of rate hikes put into place in 1H 2022 finally surface in credit markets, but it means we could be at a lull for the time being (1-2 quarters).

I think equities are going to rally on this sentiment (the fact that stocks didn’t crash spectacularly in the last 48 hours on that 9.1% print says something to me). The market is forward looking and the inflation numbers are backward looking, as much as I absolutely hate to admit it.

And while I’m happy to take a victory lap on that prediction (Disclaimer: I never predict anything correctly, so don’t get used to it), I want to now also lay out seperate game theory for the Fed going forward.

Not unlike Cameron at the very end of the movie Ferris Bueller’s Day off, when he finally decides to stand up to his father and show backbone for the first time in his life, the Fed has reached a similar opportunistic inflection point.

Given this week’s “good” (read: still absolutely dogshit 8.5% YOY) inflation print, markets have moved higher under the assumption that the Fed is going to use the data as an excuse to pivot. I think there’s an opportunity being presented to the Fed that’s profoundly different, and wanted to discuss it.

A couple of questions to ponder.

What has the Fed been desperately trying to do over the last six months?

In my opinion, it has been trying to regain its credibility with the American public, consumers and the market.

And why is gaining credibility important at this juncture?

Because part of inflation is a psychological game, and if the Fed can show the public that it has inflation under control, or at least has the means to contain it, it may help alter consumer behavior and quell inflation even further. At the very least, it will prevent panic and will appease politicians.

On an even broader scale, there are many who think that the Fed has lost significant credibility over the last couple of decades. If I were Jerome Powell, I would be keen to the idea of being able to claw back some of that credibility.

And now there’s a way that the Fed can do it. They can hold steady and continue to hike rates, as planned, despite the fact that inflation has “peaked”. Everyone is assuming the Fed is going to use the first bit of good news as a reason to pivot – hell, I have even suggested this – but they also have a very unique opportunity in the sense that they can do what is now the “unexpected” and show some backbone going forward.

Continuing to hike aggressively despite the fact that inflation is coming down would be a giant step in the Fed creating a new image for itself.

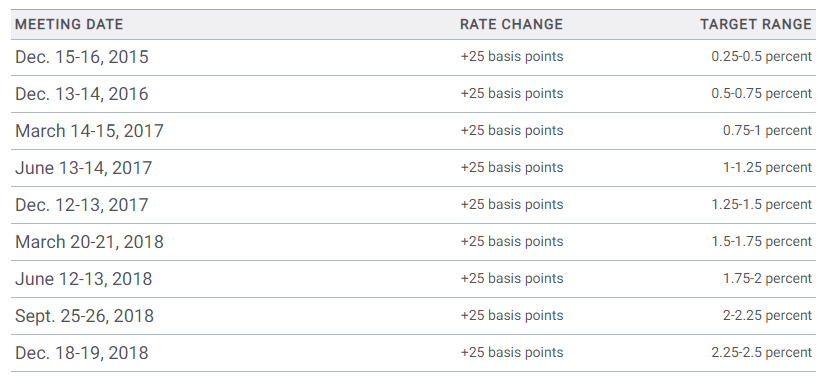

Of course, this would also exacerbate what I think is a coming trainwreck in credit markets. I described my thoughts about this in a recent piece when I noted that this year’s hikes are occurring far quicker than they did in 2018, when the market crashed in December.

For comparison, I noted in my recent piece calling out the Biden administration’s lies about the economy that the Fed hiked at nowhere near the current pace leading up to 2018. The hikes leading up to 2018 took almost 3 years to reach 2.25-2.5%.

Meanwhile, we have hiked to 2.25%-2.5% this time in just five months.

One way or another, whether the Fed hikes or decides to start pivoting soon, I still believe there’s going to be a trainwreck coming in credit markets once the aftershocks of the rate hikes that have already taken place start to make their way through the system.

At this point, the best the Fed can do is make it seem like a willing mess of their own making.

By embracing more hikes, it’ll come off as though the coming crash of the economy is what the Fed was planning for, even if it wasn’t. Last week’s job numbers, no matter how fudged they may have been, could be seen as enabling the Fed to embrace the course they are already on. In other words, the Fed may think that there have so far been no consequences of their rate hike actions.

However, the truth is that there are consequences, we just haven’t seen them yet.

I’m predicting we will feel the full force of them in the second half of this year and, as a result, markets are going to move lower from where they are rallying to this week. As such, personally, I have increased some short exposure to index ETFs to try and balance both my long and short book in my personal portfolio.

But the key takeaway from this piece is that the Fed has a chance to scrape back some of its long lost credibility given the circumstances of this past week. Whether or not they are able to find their spine for the first time since I can remember remains an entirely different question.

“When Morris comes home, he and I’ll just have a little chat.”

Disclaimer: I am an idiot and often get things wrong and lose money. I own/owned positions as disclosed above and in linked pieces. This is not a recommendation to buy or sell any stocks or securities. I own or may own all crypto/stocks I mentioned or linked to in this piece. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.